Source: LSEG Data & Analytics, 01 July 2024

Market insights

4 min read

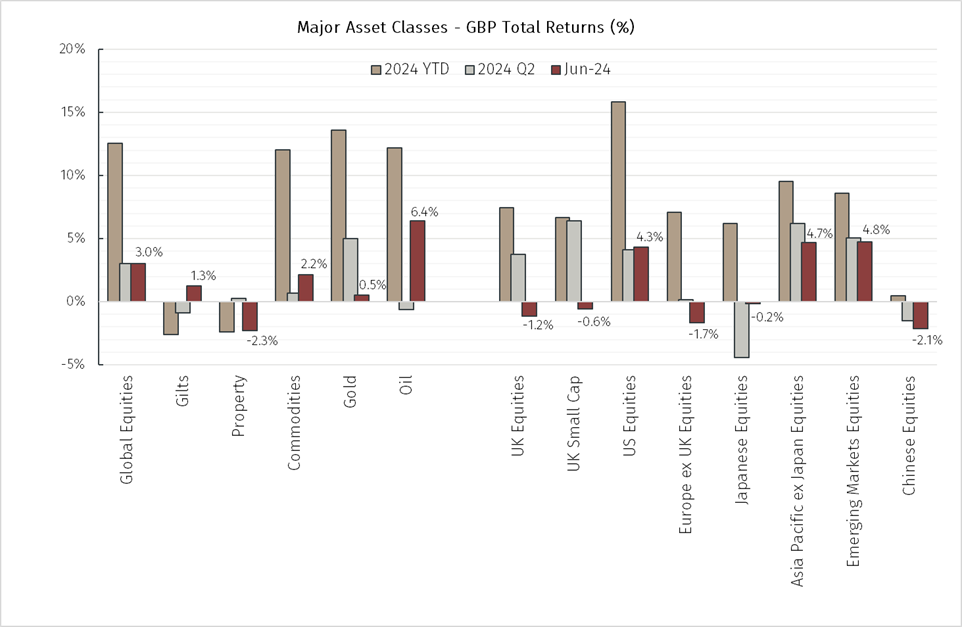

The U.S., Asia Pacific, and Emerging Markets helped spur Global equities to a positive month in June, with oil also rebounding strongly from weakness in previous months.

Source: LSEG Data & Analytics, 01 July 2024

N.B. All performance details are in GBP terms unless otherwise stated.

U.S. equities ended higher again this month as both the S&P 500 and Nasdaq logged a second-straight monthly gain, and fifth gain in the first half of the year. Behind the headline numbers, however, lies some concentration worries, as despite some intra-month volatility it was AI-linked technology companies which again led the wider market’s performance.

The Federal Reserve left the benchmark interest rate unchanged in June, with Chair Powell noting that while inflation had eased substantially, the Federal Open Market Committee still lacked confidence that the case for a rate cut was warranted. Following the meeting, Core PCE data was released in-line with expectations, showing increases of 0.1% month-on-month and 2.6% year-on-year. With this continuing disinflation narrative being combined with complementary data signalling a potential slowdown in the U.S. economy, market expectations of a September rate cut have increased, though the Federal Reserve’s policy makers maintain that they remain data dependant and no future course of action has yet been determined.

The equity story In June was not as positive on the other side of the Atlantic, however, as political risks weighed on sentiment. Following a strong performance from far-right parties across Europe in the EU elections, French President Emmanuel Macron surprised markets by calling a snap parliamentary election. While this move has not significantly altered positive views of the broader European equity outlook, it did lead to significant market volatility as market participants adjusted to try and identify potential winners and losers. European indices were dragged down by France's CAC-40 index, June's biggest underperformer among European peers, which initially erased all its 2024 gains with selloffs in major sectors like banks, energy, utilities, and property, before stabilising later in the month.

After nine months of holding rates steady the European Central Bank made their first rate cut in June, taking its key deposit rate down by 25bps to 3.75%. Despite the initiation of rate cuts long being perceived as a positive for equity markets, the impact of this first cut was somewhat muted as recent Eurozone inflation data has been slightly higher than expected, and the tone of communications from ECB committee members following the cut hinted at their next moves in July and September potentially being pauses rather than further cuts. As with their American peers, European policymakers reiterated that they remain data dependant.

In comparison with the continent, the perceived political risk in the UK has diminished, with polls still predicting an outright Labour majority following the ballot on 4 July. This lower level of uncertainty was not enough to boost markets though, with the FTSE All-Share and Small Cap indices both declining over the month. With PMI data also pointing to a loss of momentum in activity, and the services sector slowing to a seven-month low, there has been an apparent pause on many corporate spending decisions until after the election when the fiscal commitments contained within the winning party’s manifesto can be tested. These spending delays also impacted performance in the UK property market, with the FTSE EPRA Nareit UK Index declining 2.3% over the month.

For a second successive month, Japanese equities traded broadly flat, continuing a trend of softening momentum after reaching record highs earlier this year. Continued Yen weakness has been cited as a notable headwind, with Tokyo Stock Exchange data showing foreign investors sold almost JPY700bn (GBP3.4bn) in Japanese equities since the third week of June.

In China, weak economic data and doubts over the country’s recovery, particularly in the property sector, led to stocks falling in the final weeks of the month. With the Yuan also weakening and Chinese government bond yields falling back to record lows there are increased calls on Beijing to respond by easing monetary policy and/or launching a consumer stimulus programme.

Despite a somewhat volatile month in other Asian and Emerging markets, regional indices ended June in comparatively strong positive territory. The levels of volatility were most notable in India where the general election results initially provided a sharp selloff followed by a subsequent recovery, with Indian equity indices again ending the month at record highs. Elsewhere there was also strong performance in Taiwan and South Korea where AI- and chip-related stocks surged, echoing movements in their U.S. tech counterparts.

Gilts rallied in June, with yields initially dropping across the board before climbing back slightly towards the end of the month. The UK’s less uncertain political backdrop versus other key European markets, together with inflation remaining relatively cool and the belief that the Bank of England is poised to soon begin a rate cutting cycle have led to the UK becoming an attractive hunting ground for bond investors, with the 2-year/10-year yield curve disinverting for the first time since May 2023.

Among commodities, industrial metals, agriculture & livestock, and precious metals indices all fell over the month, but broad commodities indices were buoyed by a 6.4% gain in oil which more than negated the losses in other commodity assets. In addition to summer freight and shipping demand picking up, mounting geopolitical risks in the Middle East and Eastern Europe, and the potential for an impending hurricane in the Caribbean to impact refinery production have helped drive Brent and WTI crude prices higher over recent weeks.

CLOSING

As we move into the second half of 2024 and the latest round of corporate earnings, we continue to believe that attractive pockets of opportunity remain in the medium-term, however we remain cautious of longer-term reinflationary risks that services inflation, wage growth dynamics, geopolitical pressures and deglobalisation trends may fuel.

After multiple recent bouts of politically driven volatility, we also look forward to the outcomes of the UK and French elections and the prospects they may bring for unlocking further market value.

The value of your investment can fall as well as rise in value, and the income derived from it may fluctuate. You might get back less than you invest. Currency exchange rate fluctuations can also have a positive and negative affect on your investments. Please note that EFG Harris Allday does not provide tax advice. Past performance is not a reliable indicator of future performance.