N.B. All performance details are in GBP terms unless otherwise stated.

Global Market Review – June 2025

Market insights

3 min read

Global Market Review – June 2025

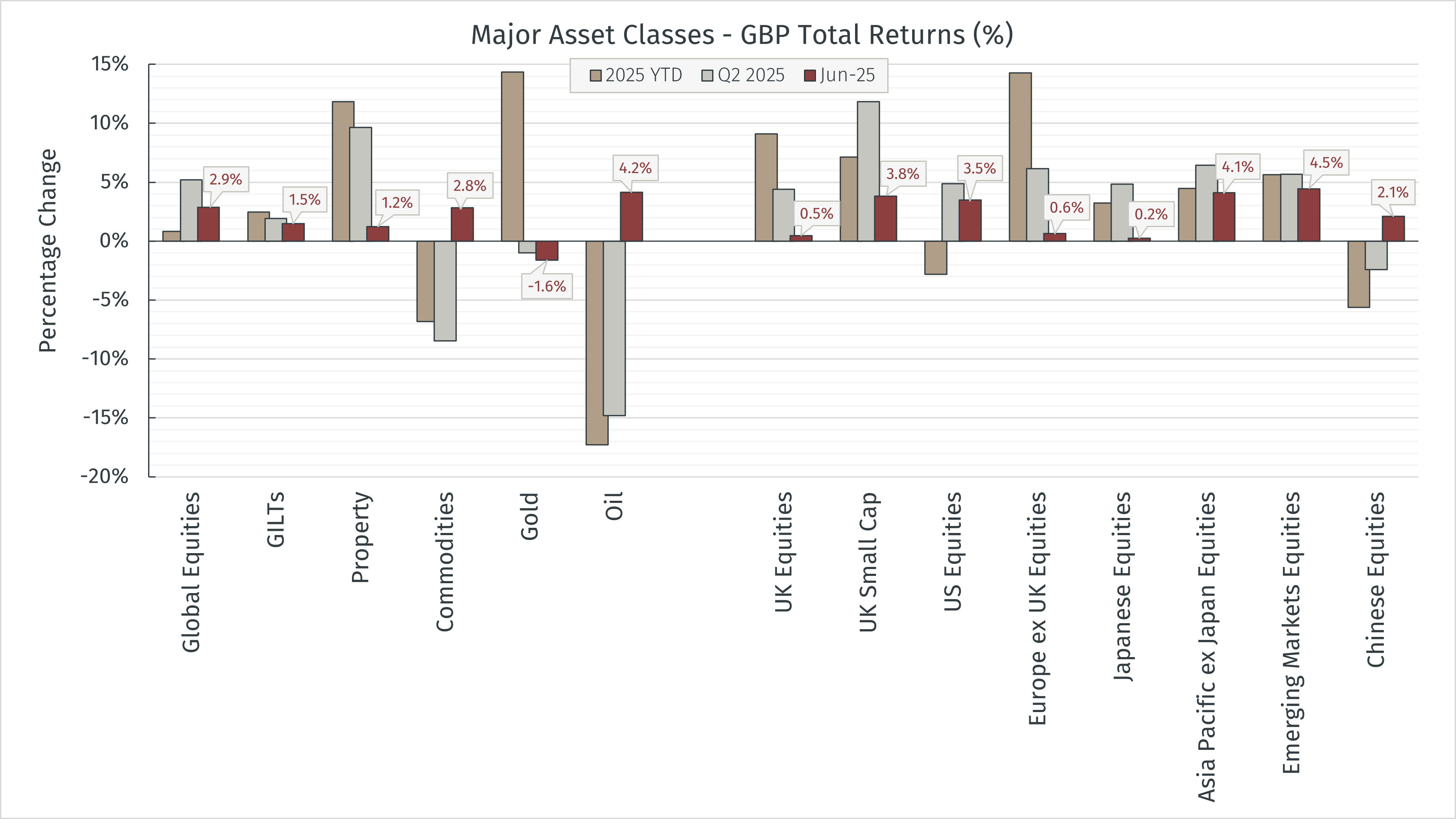

The first half of 2025 saw a clear value rotation in equity markets, with regions such as Europe and the UK which had been underperforming the US in previous years providing the strongest returns.

Source: LSEG Data & Analytics via EFG Asset Management, 01 July 2025

If there were a single phrase which dominated market parlance during 2024, it would have to be (for the second straight year) “US exceptionalism” - the idea that factors such as the scale and depth of the country’s economy and capital markets, combined with an entrepreneurial business culture and the dollar’s status as the global reserve currency gives US stocks an inherent edge over their global peers. Looking back over the past six months though, that narrative has been replaced by one of “uncertainty and volatility”.

While the year started with better-than-expected corporate earnings revisions helping to drive global equities higher during January, it didn’t take long for stagflation concerns to take hold as weakening US economic sentiment led to bond yields falling and US equity markets selling off through February and March. Worries that had initially remained US-centric then spread to other areas as concerns intensified over the potential impact that President Trump’s reciprocal trade tariffs might have on the global growth and inflation outlook.

April saw the highest levels of volatility in the wake of Trump’s “Liberation Day” tariff announcements and their subsequent 90-day pause. For example - from 01 to 08 April global equities, as measured by the MSCI ACWI Index, had provided a negative GBP total return of over 10%. From 08 April to the end of the month the same index posted a positive GBP total return figure just short of 8%.

Amid this turbulence, investor capital has found welcome homes in other equity markets, most notably Europe and the UK where a desirable mix of depressed valuations and relatively solid economic backdrops combined to attract inflows. Indeed, looking through the macro noise dominated by tariffs, performance in multiple regions has been ticking along nicely, providing decent relative returns. It is notable that the two worst performing major equity markets so far this year are the two nations at the forefront of the global trade war - the US and China.

Moving away from equities, returns in other asset classes have also been particularly prominent, albeit both positively and negatively. Commodities is a prime example of this, where the two largest components of the index - gold and oil - have seen markedly opposing returns. Despite gains seen in June on the back of geopolitical events in the Middle East, oil has faced an unfavourable supply, demand, and currency dynamic, with headwinds including the dollar weakening against other major currencies, the International Monetary Fund cutting its global growth expectations, and OPEC+ accelerating output levels. Gold, however, has continued its outperformance trend, reaching new all-time highs before plateauing slightly in Q2. Its perceived safe-haven status lifted performance in the short-term amid the elevated level of macro uncertainty, and the longer-term theme of increased central bank buying remained intact.

UK-listed Real Estate Investment Trusts have also seen somewhat of a resurgence over the first half of the year, buoyed by income-seeking investors returning to higher-yielding assets as interest rates began to fall. Consolidation and corporate activity have also supported the sector, with many trusts which were trading at larger-than-average discounts to net asset value either attracting takeover bids or adopting more shareholder-friendly corporate governance structures.

Gilt yields in the medium-to-long end of the curve have remained range-bound throughout the year, with the benchmark 10-year yield fluctuating between 4.4% and 4.9%. While these are higher than levels seen throughout the majority of 2024, it is seen as a healthy steepening of the yield curve as the short end - typified by the 2-year yield which had been rising through the second half of 2024 - has fallen back to the 3.8% to 4.0% level. This type of divergence usually supports market sentiment as a steepening of the yield curve generally forecasts growth ahead.

Looking forward, the Global macroeconomic backdrop remains positive overall but still delicate in many areas. As with the UK, the US Treasury yield curve is also trending in a steeper direction, corporate credit spreads in most developed economies are still close to 10-year lows suggesting markets are not seeing any real signs of stress in corporate finances, and inflation continues to trend in the right direction, albeit slowly in some areas.

Despite these positives, uncertainty around US tariffs remains an overhang, with very few additional detailed trade agreements made since the UK/US announced their initial framework on 08 May. While an extension to the current tariff pauses due to expire on 01 August remains a possibility, nothing is guaranteed, and the longer any uncertainty continues the larger potential economic impact it might have as companies are more likely to delay hiring and investment decisions until a clearer picture emerges.

Equity markets hate uncertainty. While we may be past peak tariff pain we believe in periods of increased volatility it is important to take a step back and focus on company fundamentals and we would continue to expect this headline-driven market to create fruitful opportunities for active investors. It is particularly difficult to consistently predict macroeconomic variables such as policy decisions accurately, not least because these are decisions made by human beings in dynamic and high-stakes scenarios. For example, although we favour a focus on market fundamentals over policy predictions, a pivot from the Trump administration towards pro-growth measures cannot be ruled out. With mid-term elections not that far on the horizon, one could reason that many Republicans wouldn’t want to see their seats at risk, and increasingly insular policies that risk causing undue amounts of short-term pain in the hope of longer-term gain might not prove popular with the electorate.

What is encouraging though, is observing the way markets and asset class correlations are behaving in between bouts of macro-driven volatility. Q1 corporate earnings were above average in many areas, and while projections for Q2 are lower than were expected at the start of the year, they still remain positive overall. There appears to be a greater focus on fundamentals when it comes to individual share price movements, traditional bond/equity correlations are being exhibited, and supply/demand dynamics remain the key focus for commodity assets.

In this environment we continue to believe in a relatively balanced asset allocation, while remaining prepared to be nimble to opportunities that may present themselves. We continue to be positive on UK, Europe, Asian and Emerging Market equities, remaining neutral in fixed income with a 3- to 5-year defensive positioning preferred. We also advocate for retaining alternative investments within portfolios for the diversifying characteristics which they bring, often being able to capitalise on unique opportunities that can emerge amid volatility.

Your investment can fall as well as rise in value, and the income derived from it may fluctuate. You might get back less than you invest. Currency exchange rate fluctuations can also have a positive and negative affect on your investments. Please note that EFG Harris Allday does not provide tax advice. Past performance is not a reliable indicator of future performance.